My 33 Expense Yrs | Morningstar

Table of Contents

The Acorn

When I started out operating at Morningstar (MORN), on Feb. 15, 1988, the mood was subdued. Reeling from stocks’ 22% reduction on Black Monday (which remains the premier solitary-working day drop in U.S. inventory-industry history), investors feared the good occasions were being around. The two equity and bond price ranges experienced loved a splendid 5-year operate from 1982 through mid-1987. Now, it appeared, normalcy would return.

As a substitute, the rocket ship arrived. The stock industry went nearly straight up, yr following calendar year, with inflation and interest premiums heading down. The fund organization followed accommodate. Historically one thing of an expense backwater–coming into the 1980s, the industry’s once-a-year revenues ended up under $500 million–mutual cash strike the mainstream. It was all incredibly interesting. I was especially content due to the fact shortly immediately after signing up for the firm, I had ignored the skeptics and placed every little thing I had (not significantly) into a totally invested inventory fund.

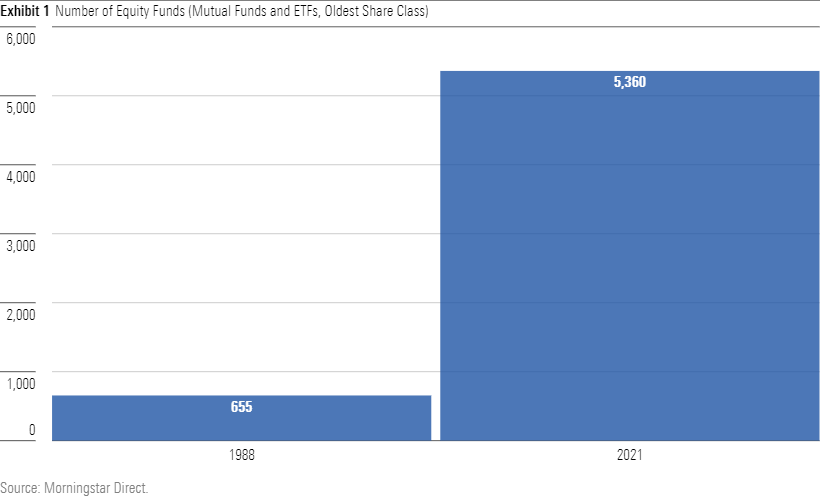

In the early many years, Morningstar analysts wrote studies on each individual present stock fund, like the $5 million Valley Forge Fund, operated by a partner-and-wife staff. (“Bernie cannot appear to the cellphone now. Can I have him connect with you back, soon after he finishes mowing the garden?”) Trying the same feat currently would demand a a great deal greater analysis workforce. Including exchange-traded resources, the equity fund depend has octupled.

Revenue, Money, Income

Despite the fact that impressive, the enhance in the quantity of resources has drastically lagged the surge in fund property. In 1988, the major mutual fund was Franklin U.S. Federal government Securities (FKFSX), which finished the calendar year with $11.7 billion. (Shut at the rear of was another bond fund, Dean Witter U.S. Govt Securities Trust (USGAX), which has given that been renamed soon after its existing operator as Morgan Stanley U.S. Authorities Securities.) Right now, 348 mutual resources and 124 ETFs exceed that determine.

The next chart, contrasting mutual-fund belongings in 1988 with all those for 1) mutual cash and 2) ETFs in 2021, efficiently conveys the tale. When I to start with arrived at perform, the industry’s advance had only just begun.

Certainly, all those numbers are not inflation-altered, but performing so would simply bump the 1988 determine to $1 trillion. That preliminary yr would continue to scarcely sign-up on the chart.

The Index Revolution

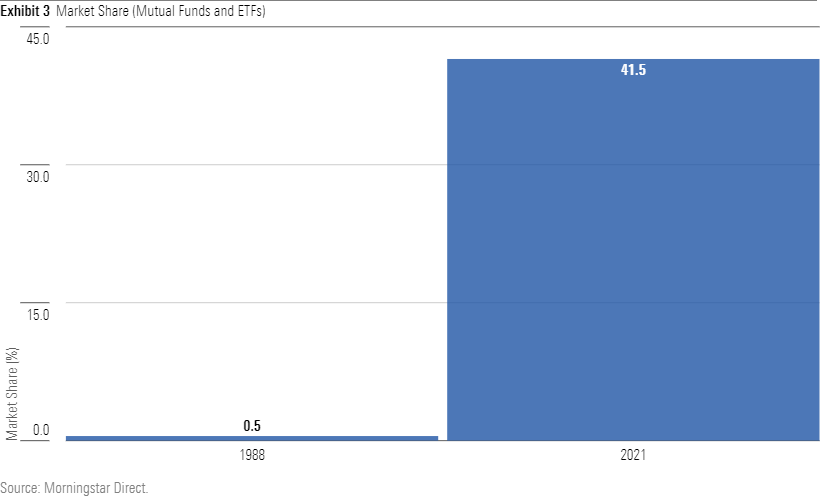

Besides amazing expansion, the other extraordinary fund progress has been the triumph of indexing. In 1988, three index funds existed: 1) Vanguard 500 Index (VFINX), 2) DFA U.S. Micro Cap (DFSCX), and 3) a brand-new entrant from Fidelity that was inevitably merged into the company’s recent featuring Fidelity 500 Index (FXAIX). (Even that listing is suspect, as DFA now states that its funds are actively managed. Nonetheless, as it called DFA U.S. Micro Cap an index fund at the time, that is where by I have put it.) In mixture, all those funds held $2 billion, producing for a current market share of a bit below .5%.

Today, index cash account for additional than 50 % of fairness fund property and just over 40% of the over-all field. That percentage surpasses my seemingly rash prediction from the early 1990s that indexers could eventually control 30% of the fund enterprise, which I had flippantly available to a Cash reporter. That grew to become the story’s primary estimate. Active administrators were being, shall we say, unamused.

The Price Is Appropriate

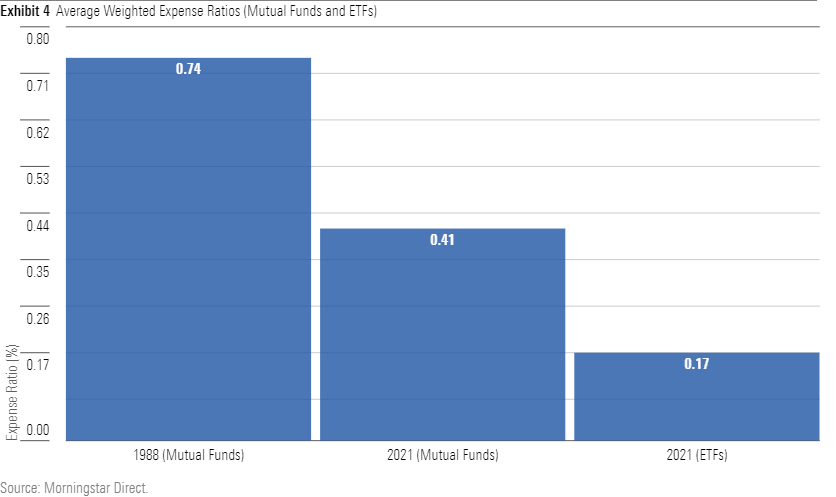

Accompanying index funds’ advance has been greater consciousness of fund costs. Again in the day, buyers who emphasized fund charges have been considered as cranks. Lifestyle was way too quick to fret about a handful of basis points. In 1993, for instance, the 5 top rated-selling mutual funds carried typical an ordinary expenditure ratio of 1.09%. When overall performance was powerful, value was not a barrier.

That angle has sharply changed, as mirrored not only in today’s most effective-seller lists– which are dominated by index funds–but also in the industry’s typical greenback-weighted price ratio, which reflects exactly where buyers now hold their monies. That has dropped sharply, from .74% for all stock, bond, and allocation funds in 1988, to .41% for mutual resources currently, and a piddling .17% for ETFs. While equally immediate buyers and fiscal advisors when downplayed the relevance of cost when evaluating money, they now position price ratios entrance and center.

Admittedly, the all-in expenses for fund investors have not dropped as considerably as the quantities would appear to show. Today’s financial advisors are compensated otherwise. While they after were being nearly solely paid out by fund providers, which embedded revenue expenses into their products, advisors now mostly cost asset-centered expenses. Hence, a lot of fund buyers pay much more than the figures propose. On the other hand, their passions now align with their advisors’. For each individual get together, the cheaper a fund, the far better.

Indeed, now that they have come to be price cut purchasers, fiscal advisors want applying institutional shares. Soon after all, why ought to their clients spend extra, when advisors can use their insider standing to organize much better offers? That the marketplace has come to be so massive, with popular advisors putting tens of millions of pounds with a one fund group, has strengthened their negotiating energy. As a result, fund corporations have increasingly created their institutional shares offered to all.

Glory Times

The fund industry’s growth enormously benefited Morningstar. My profession has as a result been blessed. When most people from my technology have not loved similar doing the job conditions, all were granted the very same terrific investment prospect. The fund organization was not by yourself in outstripping anticipations. So, too, did stock and bond performances, which simply outpaced inflation. Those people who held bonds profited. Those who held equities fared much better nevertheless. Several grew to become wealthier than they at any time would have imagined. The chart down below presents the details, for the 33.5 years that have handed considering that Aug. 1, 1988.

Regardless of whether the approaching technology will love related expenditure accomplishment remains to be observed. The consensus is or else. Most institutional researchers be expecting the soon after-inflation returns for each equities and bonds about the subsequent one third of a century to fall significantly shorter of what the most-current 3rd sent. That could well take place I don’t argue with the forecasters. Even so, it is well worth remembering that when my individual journey started, the sensible aged heads sounded the identical be aware. As Yoda would say, improper they had been.

Joyful vacations, and may possibly your fortunes be as generous as mine have been.

Editor’s Notice: The reference immediately after Exhibit 2 to the 1988 figure was corrected to trillion, not billion.

John Rekenthaler ([email protected]) has been exploring the fund field since 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s expense investigation section. John is fast to position out that even though Morningstar normally agrees with the sights of the Rekenthaler Report, his sights are his have.