")

Mongkol Onnuan

Author’s notice: All monetary knowledge in this post is introduced in Canadian bucks.

Enbridge Inc. (NYSE:ENB), a North American power transportation and distribution big is at the moment locating itself close to a 52-week reduced. Earnings traders may see the increasing dividend produce, now at 7.1%, as a rationale to scoop up shares. Interestingly, Enbridge has an substantial offering of corporate debt, and the longest dated maturity of 2083, is at present priced below par and supplying a yield of larger than 7.6%. Although a lot of superior yield buyers could not be fascinated, it truly is vital to take note that Enbridge holds an expenditure quality credit score rating, which normally features fixed money returns of nearly 200 foundation details decreased.

FINRA

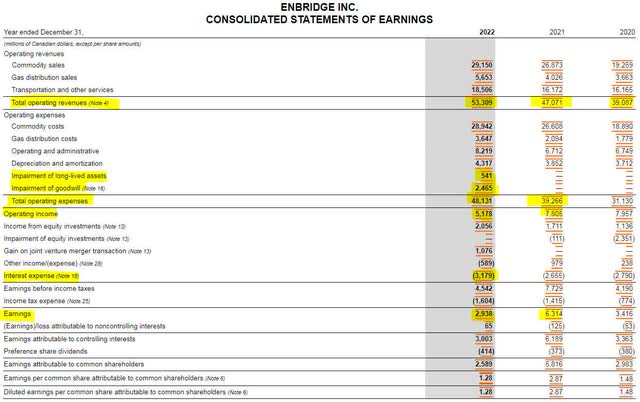

Enbridge’s operation ongoing to increase in 2022 with revenues up $6 billion from 2021. The company’s costs outpaced profits progress, but that was generally because of to the $3 billion generate off of belongings and intangibles. Had the compose offs not happened, operating earnings would have been higher in 2022 than in 2021, but however, the $5.2 billion in running revenue was ample to cover the company’s fascination bills.

SEC 10-K

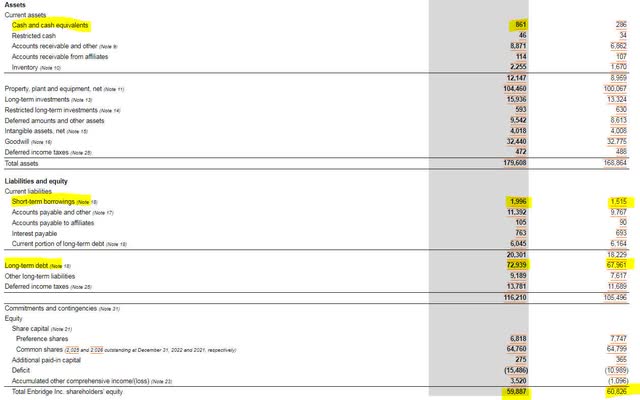

While earnings of Enbridge seemed healthy past year, the harmony sheet tells a a bit unique story. The small business enhanced its whole financial debt by extra than $5 billion and shareholder equity declined by $1 billion. The company did realize success in setting up up some money, but its recent liabilities are $8 billion greater than current property. This performing money deficit will probable lead to new credit card debt issuance or refinancing in the future 12 months.

SEC 10-K

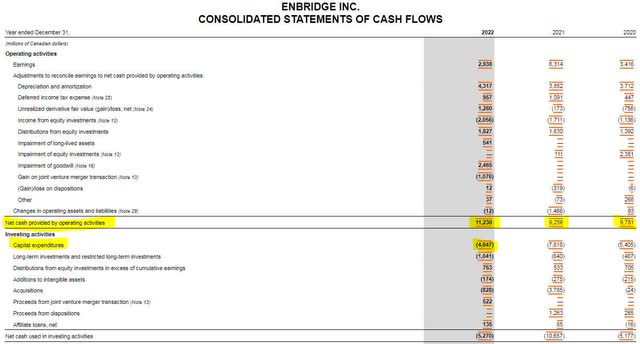

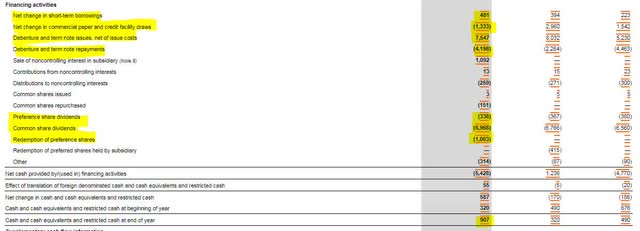

From a income circulation standpoint, credit card debt investors need to see that Enbridge can make the dollars desired to pay out down debt. In 2022, Enbridge grew operating income stream by $2 billion and generated an extraordinary $6.6 billion in absolutely free income flow. If Enbridge produced so a great deal income, why did credit card debt maximize in 2022? The solution lies in a combination of investing and funding functions. Enbridge invested $2 billion in investments and acquisitions that ended up not related to funds expenses. On leading of that, the enterprise shelled out $7.3 billion in most well-liked and frequent share dividends, and redeemed $1 billion in favored shares. The end result of these pursuits led to the enterprise needing to borrow more than $3 billion. (Take note: I feel $2 billion in more financial debt was placed on the stability sheet from other investing things to do)

SEC 10-K SEC 10-K

Under Enbridge’s current operating construction, additional capital is needed by possibly borrowing or promoting assets to sustain the widespread share dividends. Although the dividends on the most well-liked shares are quite secure, they are essentially yielding a lot less than the coupon generate on the 2083 notes. Traders in extended-term personal debt of Enbridge are having a safer security for extra earnings.

In search of Alpha

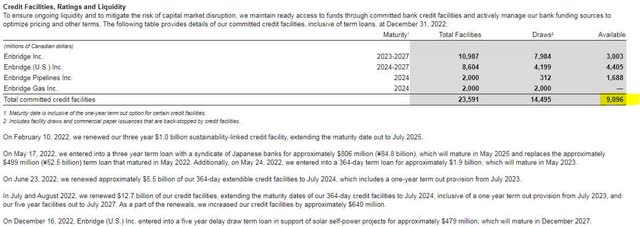

Complicating Enbridge’s foreseeable future additional is the fact that the corporation has about $14 billion worth of credit card debt maturing more than the next 2 decades. The need to refinance this financial debt in a increased fascination rate industry mixed with a functioning funds deficit is heading to set strain on the dividend. Enbridge may perhaps have to select concerning its present dividend and sustaining its credit score ranking. Luckily for personal debt holders, the corporation does have in excess of $9 billion in liquidity to get the job done with among the its present credit facilities.

SEC 10-K SEC 10-K

Even if Enbridge is downgraded into junk territory, the company’s 2083 notes are even now buying and selling at a higher return than the benchmark BB company generate. As in any scenario in lifestyle, there is a capture to what might be thought of a “as well very good to be genuine” trade. These long term notes were being underwritten with an computerized conversion covenant. In the event of a individual bankruptcy or related occasion of insolvency, the 2083 bonds would be automatically transformed into most well-liked shares. This bizarre provision is the probably contributor behind the greater return on the notes.

2083 Notes 424B Submitting

Although swings and uncertainties in the electricity markets over the following numerous yrs could enormously adjust the chance landscape for Enbridge, I believe the company’s sturdy no cost income stream can make it capable of weathering bear marketplaces. Ought to the enterprise need to have extra money stream, it could lessen frequent share dividends and not impair the worth of its bonds.

Notice: These notes are not available with all brokerage web sites, but they have been traded in increments as very low as $5,000, hence they are offered to retail holders.

CUSIP: 29250NBP9

Value: $99.00

Coupon: 7.625%

Maturity Day: 01/15/2083

Generate to Maturity: 7.63%

Credit Ranking: (Moody’s/S&P): Baa3/NR