Table of Contents

Variable-rate mortgage borrowers’ payments may climb above 40% in 2026 when they renew, Desjardins says

Article content

Lenders have been offering surprising leniency to variable-rate mortgage borrowers who’ve hit their trigger rate, but that move may be creating a “ticking time bomb” of debt when the time comes to renew, economists from Desjardins Group say.

Advertisement 2

Article content

Article content

Higher interest rates have already pushed around three-quarters of variable-rate mortgages to their trigger rate, or the point when payments only cover the interest and not the principal of a loan, Desjardins economists Royce Mendes and Tiago Figueiredo said in a recent note. Usually, banks and other mortgage holders would ask people to make more payments right away to pay down that principal. But that isn’t happening this time, which could be setting up borrowers and the Canadian economy for some rocky times ahead once renewals come due.

“The money owed still needs to be paid back,” Mendes and Figueiredo wrote. “The question is whether this is a ticking time bomb with the detonation set for a couple of years in the future.”

Advertisement 3

Article content

The full shock borrowers will feel from higher interest rates ballooning mortgage payments is getting kicked down the road because banks are waiving additional payments once people hit their trigger rate, instead adding the extra interest owed to the principal. And it’s only when the principal hits 105 per cent of the original loan that banks say they’ll come calling for those extra mortgage payments. However, no borrower is expected to reach such a lofty threshold with interest rates on hold. Indeed, the report said that would only happen if the Bank of Canada turned around and raised interest rates to seven per cent by July and kept them there until the end of next year — a very unlikely scenario. That’s good news for borrowers now, but less so in a few years down the line when mortgage terms expire.

Article content

Advertisement 4

Article content

“Many of the 75 per cent of variable-rate mortgages that have hit their trigger rate will not feel the full pain of higher rates until renewal,” the report said.

Variable-rate mortgage borrowers won’t be the only ones feeling the pain. Fixed-rate mortgages will also be impacted. Borrowers on five-year fixed terms can expect their payments to rise around 15 per cent once they start renewing in 2025 and 2026, assuming the Bank of Canada starts cutting rates at the end of this year, and its policy rate falls to 2.5 per cent by the end of 2024.

In both camps, it’s first-time homebuyers who will feel the worst shock when they renew, a result of holding less equity in their homes while also having lower incomes, the report said.

Advertisement 5

Article content

Still, the damage will be much worse for those renewing variable-rate mortgages on five-year terms. Those people can expect their payments to climb above 40 per cent in 2026, the economists estimate. Thankfully, there are ways to mitigate the impacts of higher rates, but the options are hardly affordable. For example, one way to soften the blow and keep payments where they are now is by making a lump sum payment onto the principal at renewal. But that won’t amount to a small chunk of change, and Desjardins estimates homeowners will need to put up 30 per cent of their original loan when renewing in 2026 to keep their mortgage payments steady. For someone who bought a house for $1,000,000 in 2018, with a $200,000 down payment, that amounts to a lump sum of $240,000.

Advertisement 6

Article content

If homeowners can’t afford the extra lump sum — or can’t borrow it from family — they might try keeping mortgages payments as is by extending their amortization periods. But that triggers even more problems, because most would have to extend amortization periods to more than 40 years. That’s way past the Canadian Housing and Mortgage Corp.’s 25-year amortization limit for insured mortgages. Uninsured mortgages also face a test, with banks needing to decide if such a long amortization period is “reasonable.” An amortization stretching 35 years or more probably wouldn’t meet the mark, Desjardins said.

No matter what avenue homeowners take, most will end up devoting more and more of their incomes to paying their mortgages. That will push household debt levels even higher than they are now — and they’re already the highest in the G7.

Advertisement 7

Article content

The implications from the mortgage renewal countdown are concerning, the economists said, but they don’t necessarily spell doom for the economy. “While this doesn’t put Canada on the verge of catastrophe, it will be a structural factor that could weigh on Canadian economic growth over the medium term,” Mendes and Figueiredo said.

Still, they caution that policymakers may not be factoring in just how big an impact all those renewals will have in pushing household debt levels even higher.

“The market has seemingly yet to catch on to the complications the Canadian economy will face,” they said.

_____________________________________________________________

Was this newsletter forwarded to you? Sign up here to get it delivered to your inbox.

_____________________________________________________________

Advertisement 8

Article content

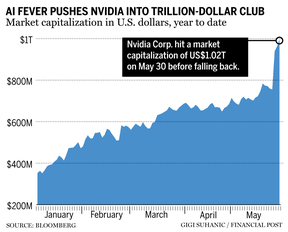

Nvidia Corp. became the world’s first chipmaker with a US$1-trillion market capitalization, joining the ranks of just five American companies with valuations that high.

The stock rose 4.3 per cent in New York trading on Tuesday, gaining a market cap of US$1.02 trillion and joining the likes of Alphabet Inc., Amazon.com Inc., Apple Inc. and Microsoft Corp. in trillion-dollar valuations. Fewer than 10 companies globally have ever achieved this level.

No other company embodies Wall Street’s current obsession with AI more than Nvidia. It has become the world’s biggest maker of the specialized chips needed to power a new generation of AI products, surpassing Advanced Micro Devices Inc. and Intel Corp. in capability just as the viral success of ChatGPT has virtually every company around the world baking AI into its operations. — Bloomberg

Advertisement 9

Article content

___________________________________________________

- The Retail Council of Canada hosts its annual retail conference in Toronto

- Today’s data: Canadian GDP; U.S. job openings and labour turnover survey, Chicago PMI

- Earnings: National Bank of Canada, Salesforce Inc., Canaccord Genuity Group Inc.

___________________________________________________

_______________________________________________________

-

How Canada’s challenger banks are navigating the banking turmoil

-

AI coming to an office job near you? Bring it on, workers say

Advertisement 10

Article content

____________________________________________________

A couple in their 40s think they could make early retirement a reality for one of them if they turn their current home into a rental and use their savings to buy a new home, but it turns out that’s not enough. We asked financial planner Ed Rempel and investment adviser Allan Small to help them adjust their dreams to reality in the latest instalment of Family Finance.

____________________________________________________

Today’s Posthaste was written by Victoria Wells (@vwells80), with additional reporting from Financial Post staff, The Canadian Press, Thomson Reuters and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at [email protected].

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the Conversation