Table of Contents

Almost a single calendar year ago, ChatGPT rolled out to the public. The ensuing synthetic intelligence (AI) growth has fuelled huge rallies in the stock market – and in some ways, even more substantial anticipations.

“While a lot of remarkable technological improvements have emerged in recent decades, the rise of generative AI could possibly prove to be the most impactful a single given that the dawn of the online,” says Brian Colello, technological innovation sector director for Morningstar.

“At present, the most important catalyst throughout know-how is generative AI,” says Dan Romanoff, senior equity exploration analyst for Morningstar Investigate Expert services.

“Software program corporations are establishing and incorporating upcoming-era AI abilities in just their answers. Cloud suppliers are introducing new providers and ramping up ability. Semiconductor companies, notably Nvidia (NVDA), are suffering from surging desire for AI and facts centre chip programs.”

Traders have latched on to this topic, and, throughout the 1st 50 % of 2023, shares for corporations deemed to have AI potential rallied strongly. Even so, a selection of key players in the area keep on being undervalued, in accordance to Morningstar analysts.

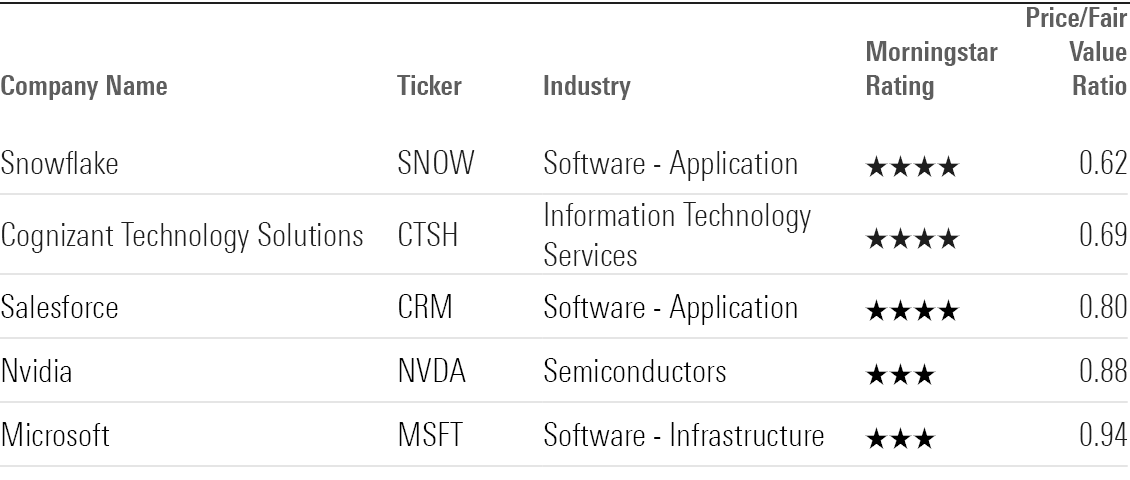

Undervalued AI Shares

• Snowflake (SNOW)

• Cognizant Engineering Answers (CTSH)

• Salesforce (CRM).

And of study course, there are two large home names that investors hunting for AI shares cannot dismiss. Each are investing at reasonable values.

• Nvidia (NVDA)

• Microsoft (MSFT).

How to Spend in AI Shares

The underlying concern for several buyers is how to participate in the AI boom. “We assume AI implementations across all forms of computer software, products and services, enterprise processes, and shopper experiences,” says Colello.

“These ongoing AI investments ought to deliver upside for semis and the similar supply chain, info management sellers, cloud computing and infrastructure leaders, software distributors, and IT expert services corporations.”

Morningstar analysts have broken the AI house down into 4 broad themes: generative AI, AI facts and infrastructure, AI software package, and AI Expert services. Within just people are more subthemes. Here are some examples of subthemes, with consultant stocks:

• Semiconductor processors – Nvidia (NVDA)

• Outsourced chip manufacturers – Taiwan Semiconductor Manufacturing (TSM)

• Chip tools distributors – Used Resources (AMAT)

• Peripheral chipmakers – Marvell Know-how (MRVL)

• Data heart infrastructure – Arista Networks (ANET).

AI Inventory Rally

The growth in AI stocks took off after the launch of ChatGPT, which lets the public to entry AI tools for their particular use. This more fuelled the present race between businesses to provide their very own variations of AI helpers within just their merchandise and platforms.

The enhance in level of popularity and desire for AI is mirrored in the efficiency of the Morningstar Worldwide Future Era Artificial Intelligence Index, which has risen 64.7% in 2023 through November 16, in contrast with the Morningstar US Sector Index‘s obtain of 18.4% about the exact same interval. Prior to this year, the index outperformed the broader marketplace more than the trailing 12-thirty day period period of time, coming in at 50.7% to the broader market’s 13.7%.

Morningstar World wide Following Gen AI

Source: Morningstar Immediate, Morningstar Indexes

Undervalued AI Shares

We screened the Upcoming Gen AI Index for prominent undervalued names. Of the 49 shares in the index, 38 are coated by Morningstar analysts. Huge 2023 rallies have remaining some in overvalued territory, these as Broadcom (AVGO) (up 77% this calendar year), Arista (up 77%), and Palantir Technologies (PLTR) (up 211%).

Till this earlier 7 days, Highly developed Micro Gadgets (AMD) was counted among the the undervalued names. But with a the latest push greater that prolonged a rally to much more than 80% gains in 2023, its inventory moved into rather valued territory. Colello notes AMD’s likely as an AI participate in: “they really should emerge as the variety-two chipmaker at the rear of NVDA for AI processors.”

On the other hand, 8 shares are however thought of undervalued, bearing 4- or 5-star Morningstar rankings. The most undervalued stock is Snowflake, which is buying and selling at a 38% low cost.

Colello highlights three of these providers as having dominant AI themes in their outlooks. We also incorporate Nvidia and Microsoft, provided their key roles in the growth of AI.

Artificial Intelligence Shares

Snowflake

• Fair Benefit Estimate: US$231.00

• Economic Moat: None.

“In just in excess of 10 several years, Snowflake has culminated into a force that is significantly from melting, in our watch. As enterprises go on to migrate their workloads to the general public cloud, significant obstructions have arisen, compromising the efficiency of details queries, creating significant details transformation costs, and yielding erroneous knowledge. Snowflake seeks to tackle these concerns with its platform, which gives all of its end users entry to its knowledge lake, warehouse, and market on numerous public clouds. We assume Snowflake has a massive runway for future growth and should really emerge as a data powerhouse in the many years in advance.

“The increase of the public cloud has resulted in an rising want to access facts from diverse databases in one location. A knowledge warehouse can do this, but it nonetheless does not satisfy all public cloud information needs – specifically in producing AI insights. Data lakes fix this problem by storing raw info that is ingested into AI versions to build insights. These insights are housed in a info warehouse to be conveniently queried. Snowflake offers a data lake and warehouse platform, which cuts out major prices of ownership for enterprises.

“Even far more valuable, in our watch, is that Snowflake’s platform is interoperable on many general public clouds. This enables Snowflake workloads to be performant for its customers with no substantial exertion to change data lake and warehouse architectures to get the job done on distinctive community clouds.”

-Julie Bhusal Sharma

Cognizant Know-how Remedies

• Fair Value Estimate: US$94.00

• Economic Moat: Slender.

“We assume Cognizant is in a very similar boat to the other IT expert services companies we address, in that they will advantage from AI because enterprises will seem to them for implementation of AI methods, which can be extremely complex and consist of much danger.

“In addition, a lot of IT products and services corporations have their own in-home AI solutions (like Cognizant’s Neuro AI option). Whilst we see the entire industry as benefitting, Cognizant stands out simply because we assume it is appreciably undervalued due to unmerited discounting for errors the organization manufactured in the past, when it was slower to produce cloud solutions.

“We assign Cognizant a slim moat, stemming from its intangible belongings and buyer switching fees connected with its expert services. Its intangible property come from its technological know-how, acquired from placing business alternatives to function throughout hundreds of firms and refining its alternatives with just about every new deployment. One instance of this can be noticed in its robust AI solutions.”

-Julie Bhusal Sharma

Salesforce

• Fair Worth Estimate: US$255.00

• Economic Moat: Huge.

“We consider Salesforce represents just one of the very best long-time period expense alternatives in software package, particularly as the corporation must give investors with a wonderful harmony concerning revenue advancement and strengthening profitability. Even as income advancement has decelerated more than time, we believe a new focus on margin enlargement ought to continue on to compound powerful earnings development for yrs to appear. We product a five-year compound once-a-year advancement rate, for total income of 12% by fiscal 2028, which we think will be pushed by strength in platform and marketing clouds, together with AI innovation.

“Salesforce has not built the very same headline-grabbing splash that some other program suppliers have in modern months with numerous AI announcements. It does not have to, as it has been an AI chief for several years. The business initially launched Einstein in 2016, and it has given that grow to be embedded in the firm’s system, and it’s been readily available in all the company’s clouds for many years. Einstein presently would make 194 billion predictions each individual day, in contrast with 8.5 billion Google world-wide-web lookups per day, so the scale concerned is now huge.

“We see the arrival of AI Cloud as vital for both equally Salesforce and its customers, as it will allow clients to use huge language types that are delivered by Salesforce, brought by themselves, or from third-party providers, this sort of as OpenAI. To progress trust – which we believe is significant to safe buyer purchase-in – AI Cloud makes use of approaches to avert organization data from staying considered by Salesforce and from remaining ingested into generic LLMs, thereby turning into portion of the larger sized AI.”

-Dan Romanoff

Nvidia

• Fair Worth Estimate: US$480.00

• Economic Moat: Vast.

“Nvidia has a huge financial moat, many thanks to its obvious management in GPUs and the components and software program instruments needed to enable the exponentially increasing sector about AI. In the prolonged run, we count on tech titans to attempt to obtain second sources or in-property answers to diversify absent from Nvidia in AI, but most probably, these attempts will chip at but not supplant the company’s dominance.

“Nvidia took an early lead in AI GPU hardware, but far more importantly, it created a proprietary computer software platform, Cuda, and these equipment let AI developers to create their styles with Nvidia. We believe that Nvidia both equally has a hardware lead and added benefits from substantial buyer switching costs around Cuda, producing it not likely for an additional GPU seller to arise as a leader in AI training.

“We assume Nvidia’s potential clients will be tied to the AI market, for greater or worse, for fairly some time. We hope main cloud vendors to go on to devote in in-dwelling semis (with Google and Amazon major the way), when CPU titans AMD and Intel will work on GPUs and AI accelerators for info facilities. Having said that, we look at Nvidia’s GPUs and Cuda as the sector leaders, and the firm’s substantial valuation will hinge on regardless of whether (and for how extensive) the organization can keep ahead of the pack.”

-Brian Colello

Microsoft

• Reasonable Price Estimate: US$370.00

• Economic Moat: Extensive

“Microsoft is one of two public cloud vendors that can provide a huge wide range of platform as a service/infrastructure as a support options at scale. Dependent on its expenditure in OpenAI, the company has emerged as a chief in AI. The company has also relished fantastic achievement in upselling people on higher-priced Business office 365 variations, notably to consist of highly developed telephony capabilities. These elements have put together to generate a extra centered business that delivers remarkable income progress with substantial and expanding margins.

“We consider Azure is the centerpiece of the new Microsoft. Even nevertheless we estimate it is presently an around $58 billion small business, it grew at an remarkable 30% fee in fiscal 2023. Azure has various distinctive rewards, which include that it offers clients a painless way to experiment and transfer pick out workloads to the cloud, making seamless hybrid cloud environments. Considering that current buyers stay in the exact Microsoft natural environment, applications and info are easily moved from on-premises to the cloud.

“Microsoft can moreover leverage its huge set up foundation of alternatives as a touch point for an Azure move. Azure is also an fantastic launching issue for secular tendencies in AI, organization intelligence, and the World wide web of Points, as it carries on to start new solutions centered all over these broad themes.

“We raised our honest price estimate for Microsoft to $370 from $360 right after it claimed excellent benefits and guidance for its fiscal initial quarter of 2024. Shares are up adhering to earnings, leaving the inventory just inside 3-star territory. Microsoft is a title we want to personal, but we really don’t see a large valuation layup.”

-Dan Romanoff

AI Stock Effectiveness

Supply: Morningstar Immediate, Morningstar Indexes

")

Stocks That Glance Prepared to Break up")